This is a short-form life insurance needs analysis system you can use in just ten minutes to achieve the same answers as an inch-thick comprehensive analysis, without the fancy full-color report. Here’s how it works:

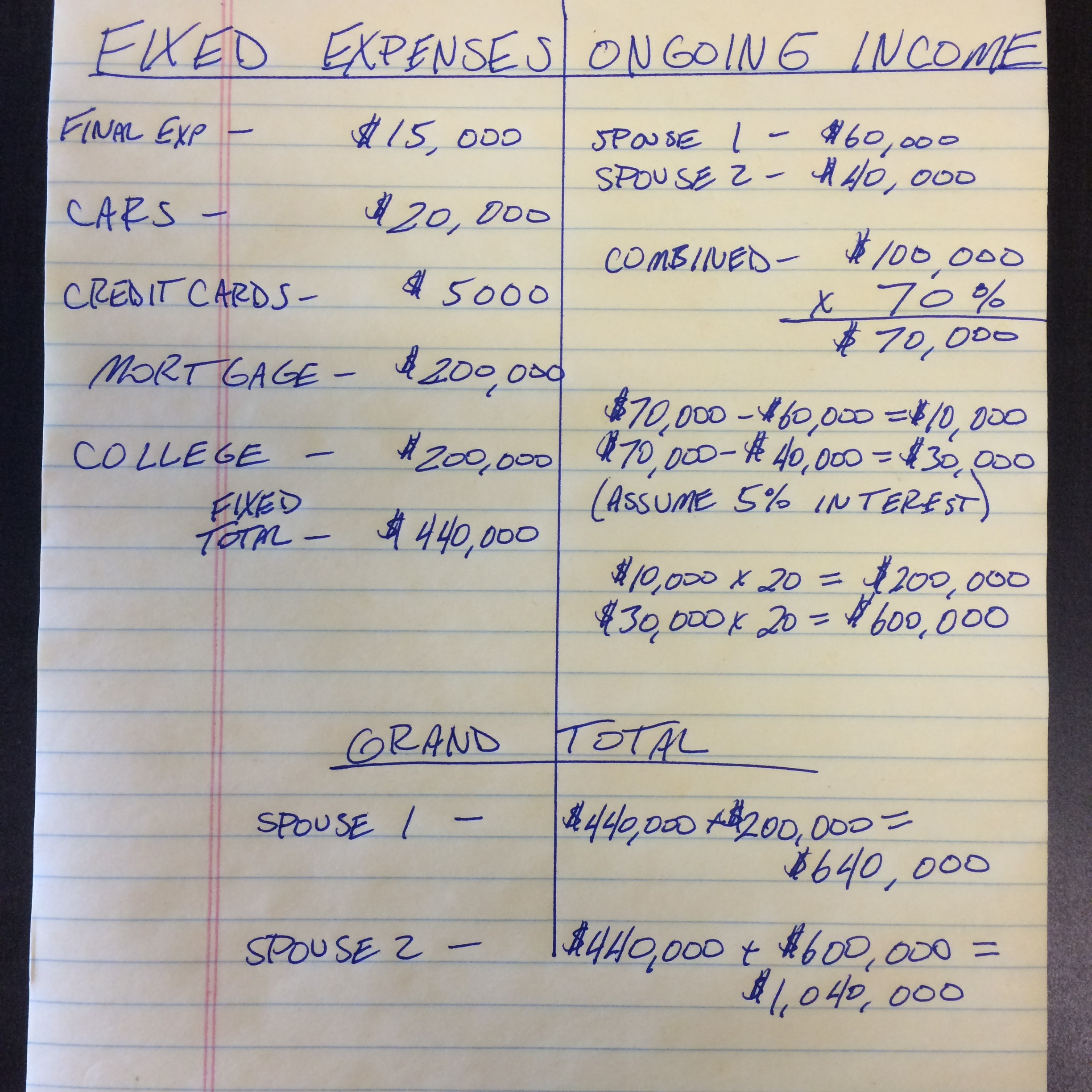

Take a piece of paper and draw a vertical line down the middle. The heading on the left should be FIXED EXPENSES. The heading on the right should be ONGOING INCOME NEEDS. Start on the left with the FIXED EXPENSES column. Everybody needs funds to cover their final expenses (casket, burial, cremation). If you have had a loved one pass away recently you may know the current expenses in your area. If not, I suggest $10,000-$20,000. Next, list all debts you would like to pay off upon your death. The largest will likely be your mortgage if you own your home. Automobiles and credit cards usually make up the remainder. If you have children, you can include an amount to cover college tuition in this column.

Add up the numbers on the left column. If all those items were paid off, would your family be able to maintain their standard of living on your spouse’s income? Most families still need some additional income. If you are not sure, a good rule of thumb is that your spouse and children will need roughly 70% of your former combined income to maintain their standard of living. Most families need some additional income. We will take a look at those ONGOING INCOME NEEDS in the right column.

Let’s use our 70% number in the right column. Add your incomes and take that number times 70%. That’s the income your family still needs if one of you passes away. For example, if you make $60,000 and your spouse makes $40,000, one remaining spouse would still need $70,000 total. That translates to an additional income need of $10,000 if the spouse making $40,000 dies, or $30,000 if the spouse making $60,000 dies. We need to make up the difference and get back to the $70,000 total.

How can we use life insurance to provide that income stream? I like to use easy math. Let’s say we need to generate $30,000 per year. A lump sum of $300,000 earning 10% interest would generate $30,000/year without reducing your principal ($30,000 times 10). A lump sum of $600,000 earning 5% interest would do the same (half the interest rate, double the lump sum). You could split the difference if you expect a rate of return in between, $450,000 at 7.5% interest. Use your judgment as to what return you would reasonably expect to earn based on your past investing experience.

Once you have the numbers from both columns, add them together to arrive at the amount of coverage your family needs. Here is an example using the numbers discussed above: